{kind=link}

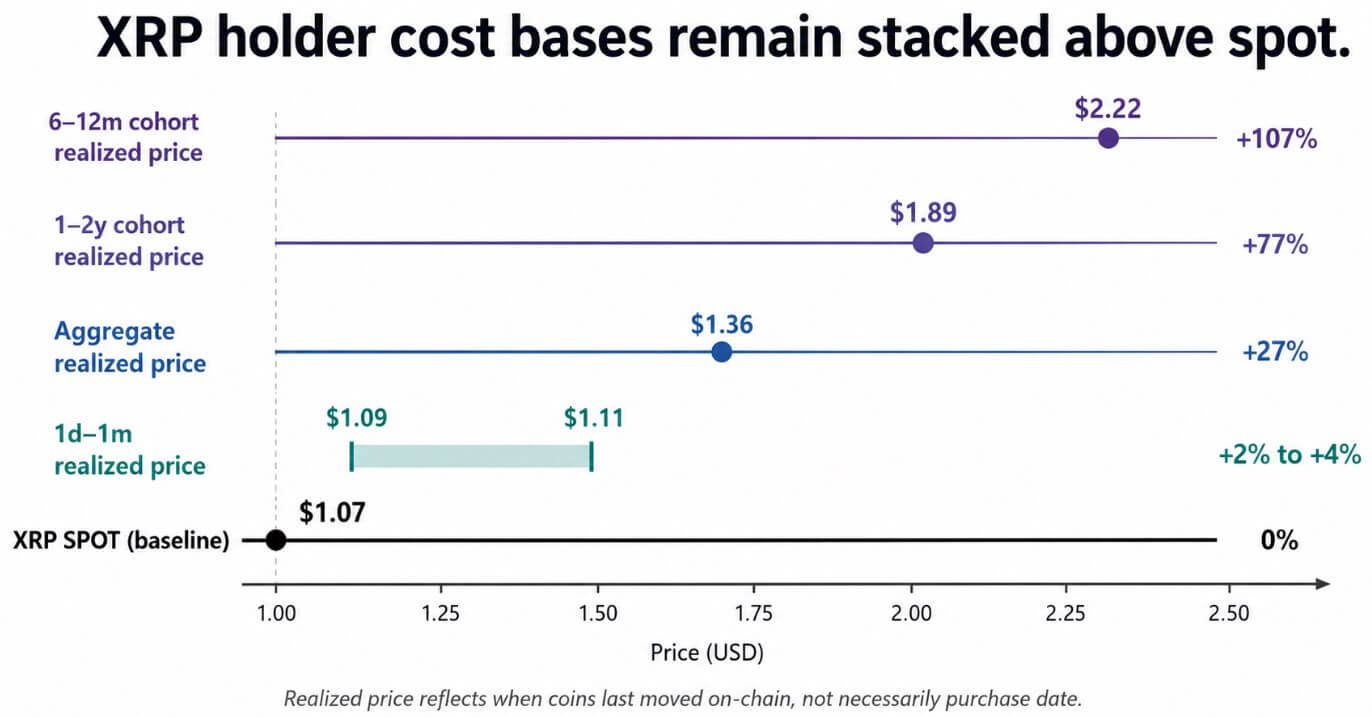

Glassnode reported that XRP holders who bought between 6 and 12 months ago have an average cost basis near $2.22, roughly 52% above the token’s price of $1.08 on July 14, and far above the $ 1.09-$1.11 realized price for coins bought in the past month.

XRP perpetual funding spanned a 2.6-basis-point range as of July 12, running from -0.016% on Kraken, through -0.003% on Coinbase, -0.002% on Bybit and Crypto.com, and roughly 0% on Binance, up to +0.005% on Gate, +0.006% on Hyperliquid, and +0.010% on Bitget and Huobi.

How far underwater each cohort sits

Glassnode calculates realized price as the average price at which the circulating supply last moved on-chain, with the duration of each cohort’s holding tracked separately.

The one- to two-year cohort has a realized price near $1.89, about 43% below the current spot price and roughly 77% short of breakeven.

The 6-to-12-month cohort needs about 107% from here to reach its $2.22 average cost, while XRP’s aggregate realized price is $1.36.

Glassnode’s aggregate NUPL reading, which measures unrealized profit against unrealized loss across the tracked supply, sat near -0.252, meaning losses outweigh gains across the token’s entire holder base.

The funding rate is a periodic payment between long and short positions, moving from longs to shorts when the rate runs positive and reversing direction when it runs negative, a mechanism meant to keep perpetual futures prices tethered to spot.

The eight venues tracked by CoinGlass split evenly on July 12, four negative and four positive, with no shared directional lean across the market.

CoinGlass cautions that funding varies by venue due to user composition, margin preferences, contract volume, and each exchange’s own mark-price system, and that the metric works best alongside open interest, volatility, and liquidation data, with the funding number alone telling only part of the story.

Even with that caveat, a 2.6-basis-point spread between the most negative and most positive venues describes traders making opposite bets on the same asset at the same time.

| Funding side | Venue | XRP perpetual funding |

|---|---|---|

| Short-biased / negative | Kraken | -0.016% |

| Short-biased / negative | Coinbase International | -0.003% |

| Short-biased / negative | Bybit | -0.002% |

| Short-biased / negative | Crypto.com | -0.002% |

| Neutral | Binance | ~0.000% |

| Long-biased / positive | Gate | +0.005% |

| Long-biased / positive | Hyperliquid | +0.006% |

| Long-biased / positive | Bitget | +0.010% |

| Long-biased / positive | Huobi | +0.010% |

What a move in either direction would trigger

CoinGlass puts XRP’s 24-hour futures volume at over $1.7 billion, compared with a spot volume of about $290.4 million, a ratio of about 5.9 to 1.

Open interest sits near $2.3 billion, down from June’s levels, and the volume gap shows derivatives still drive most of the turnover investors actually see day-to-day.

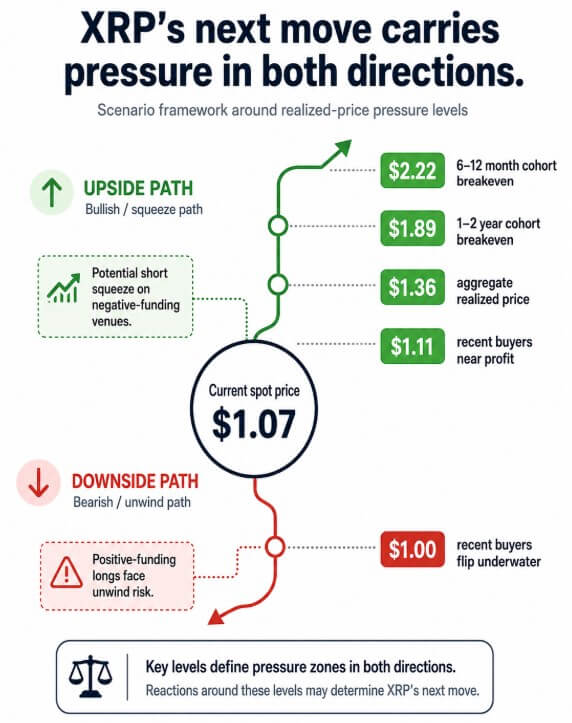

A sustained move above $1.11 would first put the most recent buyers into profit, and a run toward the $1.36 aggregate realized price would start to repair the broader holder base.

That same move could squeeze the negative-funding venues, forcing short-biased traders to cover as the price climbs past the cost basis that recent buyers are watching.

A rally can reward newer buyers well before it repairs the oldest ones, since the $1.11 and $1.36 levels sit far below the $1.89-$2.22 cohort wall.

A decisive break below $1 would flip recent buyers into losses for the first time and push older cohorts deeper underwater.

That same move would test the positive-funding venues, where traders are already paying to stay long, forcing the most exposed positions to unwind as losses compound on both sides of the market.

The backdrop investors are trading against

The Federal Reserve held its target rate at 3.50% to 3.75% on June 17, citing uncertainty tied to the Middle East conflict and inflation partly linked to energy supply shocks.

Renewed US-Iran hostilities on July 13 pushed Brent crude up 2% to $77.60 and supported the dollar as a safe-haven asset, with money markets pricing in 37 basis points of Fed tightening for the year, a backdrop that tends to tighten liquidity for higher-beta assets like XRP.

US-traded spot XRP ETFs recorded about $7.2 million in net outflows during the July 6-10 week, led by a $7.29 million outflow from Bitwise’s fund, the same week US spot Bitcoin ETFs pulled in about $197 million and ended an eight-week run of redemptions.

Glassnode’s own cost-basis methodology comes with a caveat worth keeping in mind when reading this data: realized price tracks when coins last moved on-chain, a signal that can capture transfers and custody changes alongside ordinary buying.

The cohort and funding splits still describe a market few investors would call settled.

XRP’s next move carries a specific test in either direction: clearing $1.11 and then $1.36 before it reaches the coins still priced near $2.22 on the way up, or holding below $1 before positive-funding venues start unwinding on the way down.