{kind=link}

Bitmine Case Study:- The idea of companies holding digital assets as treasury reserves is still relatively new. While corporate crypto treasuries began appearing roughly two to three years ago, their long-term survivability has remained a persistent question.

Can companies survive by simply holding digital assets on their balance sheets?

This debate has intensified as more firms across crypto and Web3 attempt to build businesses around large token treasuries. Critics argue that passive holdings expose companies to extreme volatility while offering little operational value beyond price speculation.

This question becomes even more relevant as the scale of corporate crypto treasuries continues to grow.

BitMine – The Ethereum Treasury Case Study

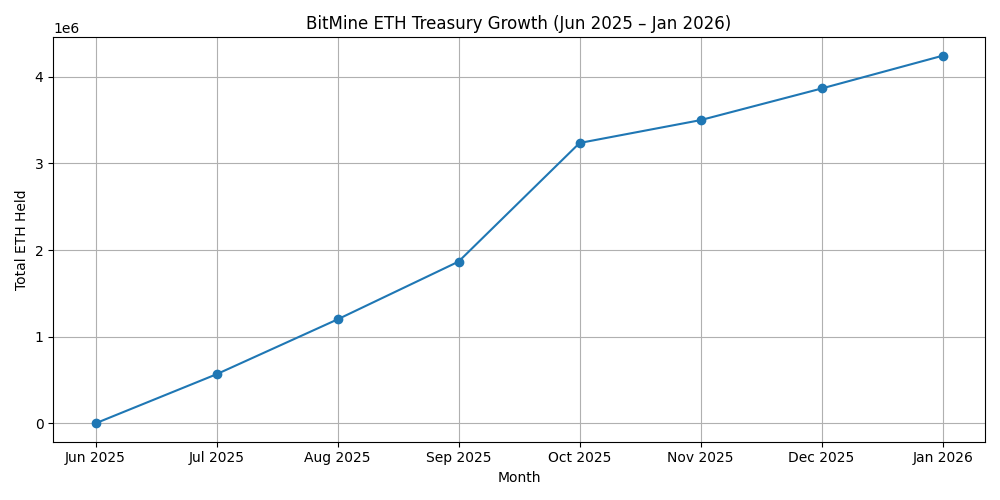

One of the most striking examples today is BitMine Immersion Technologies, a Tom Lee-led public company that has rapidly accumulated one of the largest corporate Ethereum treasuries in the market.

As of early 2026, BitMine holds millions of ETH, 4.23 Million, to be precise on its balance sheet. This places it among the most aggressive corporate accumulators of Ethereum globally. This Bitmine DAT case study which critically analyses its revenue growth and key facts over the last quarters reveal an interesting fact. Bitmine has not generated any signficant profits from its ETH holdings.

This comes as most of its revenue drivers continue to be mining and infrastructure services. However, Bitmine’s ETH Strategy goes beyond P&L statements as the case study reveals.

Also Read: How Securitize Build a $4B Tokenization Platform

How BitMine is Making Holding Ethereum Productive

The company’s strategy is not stopping at just about holding Ethereum.

Instead, BitMine is attempting something far more ambitious, turning its treasury into a productive financial engine.

The company has begun staking a large portion of its ETH holdings, capturing protocol-native yields and expecting to geenrate $373-396 million in annual income. It is also expanding validator operations with MAVAN launch and exploring additional on-chain revenue streams such as tokenization and apps.

This shift represents a broader strategic pivot in the search for survivle business model for the digital asset treasury companies. moving from passive holding to active productization of crypto assets.

In other words, the Bitmine’s case study reveals significant fidnings – future of corporate crypto treasuries may not lie in accumulation alone, but in Bitmine’s strategic DAT play.

What you’ll learn in the full case study:

- A detailed, source-backed timeline of accumulation and staking activity.

- On-chain evidence that corroborates public filings and investor disclosures.

- A conservative revenue build showing how staking + MEV + short-duration cash could change EBITDA profiles.

- Scenario analysis: what happens to the company at −30%, −50% and −70% ETH price moves.

- A practical checklist for other firms trying to “productize” treasury assets.

Want the whole picture?

This summary scratches the surface. The full CoinGape case study walks through the numbers, the on-chain evidence and the strategic choices in detail and it leaves some questions open intentionally.

If you’re following corporate ETH treasuries, staking economics, or the next big wave of productized on-chain yield, the full piece is worth your time.

Investment disclaimer: The content reflects the author’s personal views and current market conditions. Please conduct your own research before investing in cryptocurrencies, as neither the author nor the publication is responsible for any financial losses.

Ad Disclosure: This site may feature sponsored content and affiliate links. All advertisements are clearly labeled, and ad partners have no influence over our editorial content.